For a long time, many real estate brokers and investors have believed that the capitalization (CAP) rate was the best indicator of the value of a piece of real estate.

However, real estate values cannot be boiled down to a simple CAP rate. There are too many variables that need to be considered in establishing a value of commercial in addition to the CAP rate.

These variables also affect property valuations:

- Age of building

- Condition of building

- Quality of building (concrete tilt, concrete block, metal, wood, etc.)

- Location

- Above or below grade

- In a small town

- In a metropolitan area

- Flood plain

- Length of lease terms

- Quality of tenants

- Kind of lease (gross, modified gross, NNN, absolute NNN)

- Quality of leases, ie. a two-page homemade lease or a sophisticated lease (the more sophisticated, the less risk for the investor)

- Population growth or shrinkage

- Local regulations (zoning, for example)

- Rent controls

- Property taxation rules in that submarket

- Weather patterns (fires, hurricanes, tornadoes, flooding)

- Risk of pollution, water, hydrocarbons, etc.

- The economy

- Interest rate variability

- Potential leasing rates

- Variable property management fees

- Tenant improvements

- Potential future capital retrofits (plumbing, electrical, asphalt, roofing, etc.)

- Vacancy rates and estimated length of potential vacancies

- Current market conditions

- And most importantly, cash flow

The Importance of Real Estate CAP Rates Vs. Cash Flow

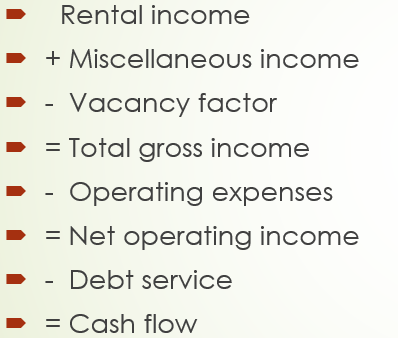

Real estate gains value in these four ways: debt reduction, depreciation shelter, appreciation and cash flow.

Cash flow is one of the most important variables when establishing a value for a commercial investment property. In simple terms, property income minus property expenses minus debt equals cash flow.

This is a simple overview. Unfortunately, even using this basic analysis, many properties do not cash flow well enough to buy. Former rules of thumb indicated a positive cash flow of over 5% might make for a reasonable deal, if you included a vacancy rate, property management and reserves into the expense components.

This may sound very conservative, but the real estate market is never in stasis. In addition, there are many new variables we need to consider. For example:

- Rent control for residential properties

- Online shopping for retail properties

- The massively increasing costs of labor and materials

- The closing of hundreds of retail stores like Advance Auto, Rite Aid, Family Dollar, Macy’s, Pizza Hut, Seven – Eleven, Grocery Outlet and 99 Cents Only are a signal that the tension between online shopping and retail shopping is building. Clearly, competition also plays a role in this picture and it’s hard to have multigenerational growth in any business without extraordinary leadership. But having a broker tell you that a 10-year lease does not need reserves or a vacancy rate is a broker that has never invested in real estate for themselves.

- Outdated industrial buildings

- Interest rate and down payment variability. With 40% down requests by financial institutions, the concept of leverage has become a weaker part of the real estate investing landscape.

- Tax rates and increases (different in every state)

- Plus, the above list of property variables

What Can Real Estate CAP Rates Really Tell Us?

Low CAP rates are being used as a sales tool to entice buyers, but CAP rates are a small part of a larger purchase analysis and should be viewed that way by investors. They are simply indicators of value showing a relationship of net operating income (NOI) to the sales price. This cannot be construed to tell the picture of a total real estate deal. It’s high time for investors to use cashflow analysis and a thorough due diligence process to assess investment risks and variables that establish a reasonable sale price.

There are many reasons property sales are currently slow, and they boil down to challenging seller expectations and high down payments required by lenders in our current interest rate environment. Deals are occurring when the seller agrees to a significant value write down.

Despite the stronger start to 2026, pacing slowed heading into late spring. April 2026 experienced a 33% decline compared to an unusually strong April 2025, highlighting that the market recovery is stabilizing rather than skyrocketing—see data references below.

For the market to pick up momentum, sellers and lenders must change their attitudes. In the meantime, CAP rates are probably not the best measure to use when estimating real estate values. Unfortunately, it seems that the current CAP rate environment may have outlived its usefulness.

Maybe the time has come for a change in the way we calculate real estate valuations. In any case, overpriced listings and unrealistic CAP rates will not encourage buyers to pull the trigger.

A Few Further References:

- MSCI Real Capital Analytics (RCA) – Q1 2026 Capital Trends: Source for the $110.7–$113 billion total investment volume figures and the baseline 18% year-over-year Q1 volume growth. This report also provided the breakdown for the office investment rebound ($20.5 billion, up 39% YoY) and industrial liquidity ($31 billion, up 27% YoY).

- CBRE U.S. Capital Markets Figures (Q1 2026): Confirmed the overall surge in commercial real estate investment volume to roughly $117 billion (a 19% YoY baseline increase) and detailed the expansion of inbound cross-border capital (+18%).

- CoStar Group / Commercial Repeat-Sale Indices (CCRSI) Q1 2026 Market Report: Source for the value-weighted price indicators, smaller vs. larger property size trends, and sector-by-sector volume distributions (noting the divergence where general commercial volume rose roughly 20%).

- Altus Group – U.S. Commercial Real Estate Transaction Analysis (Q1 2026 & Q4 2025): Provided the data regarding shifting median deal sizes, price-per-square-foot benchmarks (e.g., multifamily leading at ~$150/SF), and historical context for full-year 2025 volumes ($560.2 billion baseline).

- Mortgage Bankers Association (MBA) Commercial/Multifamily Quarterly Forecast: Source for lending liquidity trends, including the projected 27% increase in commercial mortgage originations ($805 billion total) for 2026.