Many investors find purchasing a new commercial property easy, but recording a fixed asset purchase in QuickBooks can be complex and unclear.

In this article, we will discuss best practices and walk you through the steps to record the purchase of a fixed asset in QuickBooks. First, let’s begin with defining a fixed asset.

What is a Fixed Asset?

Fixed assets are property that a company owns which have a useful life of greater than one year. Examples of fixed assets include land, buildings, machinery, & some office equipment. Fixed assets cannot easily convert into cash. For instance, stocks, bonds, and other long-term investments do not qualify as fixed assets because companies can easily convert them into cash. Generally, you can depreciate fixed assets, except for land. In accounting, fixed asset accounts appear on the company balance sheet.

Understanding Fixed Asset Accounting in Real Estate

Before jumping into journal entries, it’s helpful to know how fixed assets function in real estate accounting. Simply put, fixed assets in QuickBooks are long-term assets your business possesses, such as buildings, land, or large equipment, that generate worth in the long run as opposed to being sold quickly for money.

As you track these properly, you have an accurate view of your company’s financial situation and future development. With fixed asset software provided by QuickBooks, you can track your property purchases, keep on top of depreciation, and stay accounting standards compliant, without having to balance multiple spreadsheets.

Having accurate documentation of your assets also proves useful when selling, refinancing, or doing taxes. Think of it as the backdrop to your financial story; every tidy record tells a piece of how your real estate investment is growing.

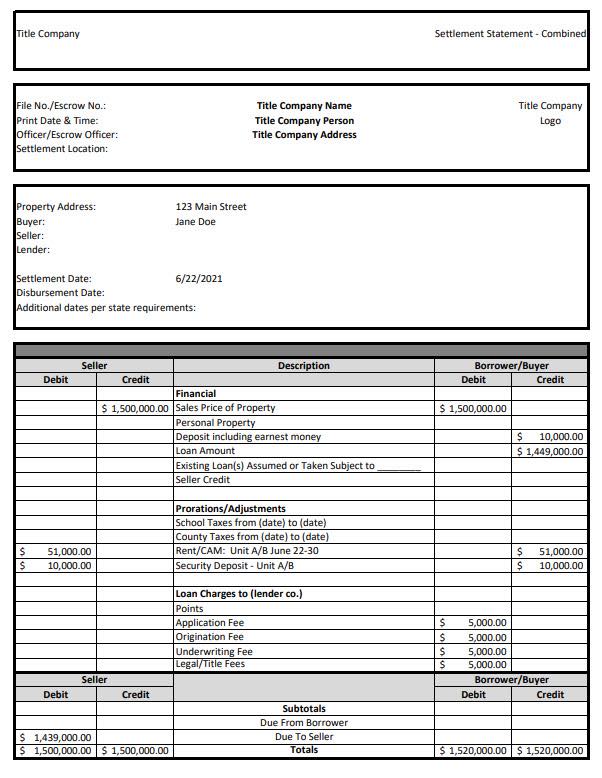

The Settlement Statement

One of the most common questions in commercial real estate is:

How do I enter a building I just bought into QuickBooks?

The best way to record the purchase of a fixed asset in QuickBooks is to use the closing documents from the sale. Typically, people refer to it as a Settlement Statement. Others call it a Closing Disclosure (CD). It is often called a HUD statement (because the U.S. Department of Housing and Urban Development requires it). Whatever you call it, what you need for accounting purposes is the breakdown of any money transferred during the transaction.

A title company’s job is to divide the expenses correctly between the two participants in a real estate transaction. The seller will pay their prorated portion of real estate taxes, rent, utilities, etc., based on the transaction date, and the borrower may have some of the expenses. Using the Settlement Statement to set up your new building in QuickBooks provides almost a “cheat sheet” for entering the transaction. We will use the Settlement Statement below as our example for building the Journal Entry in QuickBooks.

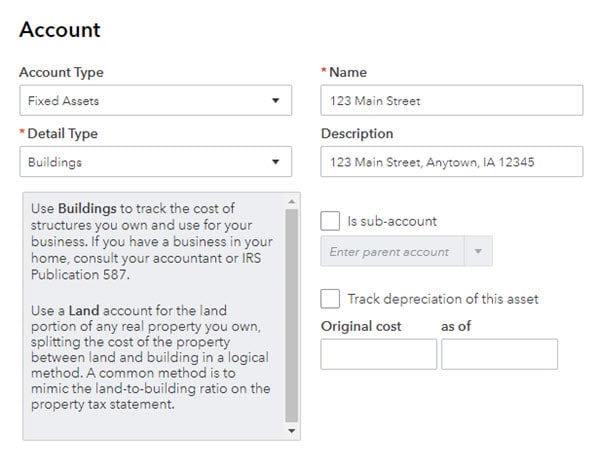

Add Accounts for the New Property

Before you begin recording the purchase of a commercial property in QuickBooks, make sure to set up two new accounts.

- Fixed Asset Account

- Loan/Notes Payable Account

To create a new account, go to Accounting > Chart of Accounts > New. Or go to the NEW button on the top left and click on Journal Entry. When you begin typing an account name, a green plus will appear, and you can add an account from there.

Add New Fixed Asset Account

We need to create a new fixed asset. For buildings, I recommend using the address or a parcel number for unique identification. If you would like to track depreciation, check the Track depreciation of this asset box. (Ensure to discuss depreciation with your accountant as not all assets can be depreciated).

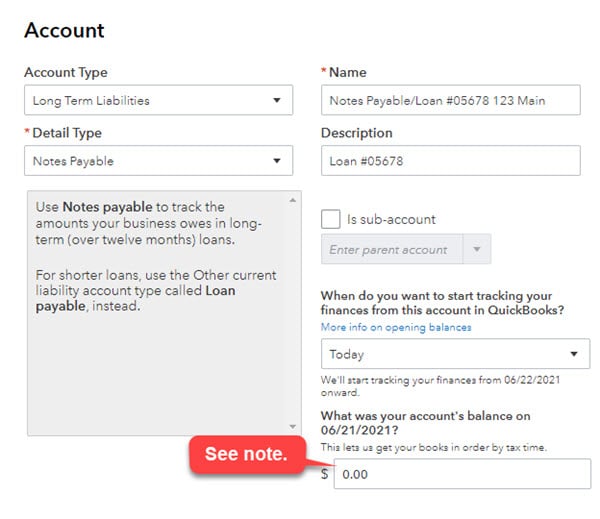

Add New Loan/Notes Payable Account

Next, set up a new Loan/Notes Payable account if you purchased the property with any kind of loan.

NOTE: I prefer to start with a zero balance when creating the Loan account. The balance amount entered here debits the opening equity in a background transaction. Entering zero allows me to create a Journal Entry with the full amounts and not have to worry about a double entry from the amount entered here.

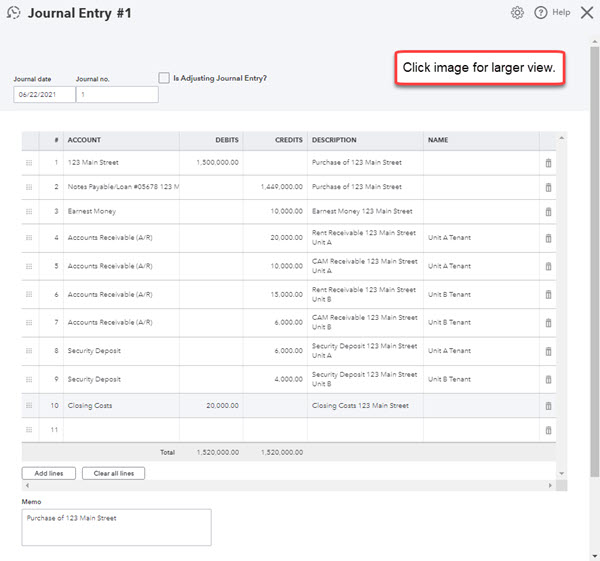

Create a Journal Entry for Recording the Purchase of a Fixed Asset

To create the Journal Entry, go to the NEW button on the left top corner to create a Journal Entry.

NOTE: The information below is how a typical Journal Entry will be recorded. As always, check with your accountant to ensure you are recording it correctly for your particular circumstances.

Line 1: Enter the Purchase Price

Your building is a fixed asset, and your purchase price is typically the book value. To increase an asset, you use the debit column. See the example below.

NOTE: If the purchase price includes land, you will want to separate it out. Buildings can depreciate, but land does not. Check with your accountant for more information.

Line 2: Enter the Loan Amount

“Loan/Notes Payable” is a liability account, and it will increase the company’s liability, so it is placed in the credit field.

Line 3: Earnest Money

Earnest money typically is a check made out of your cash/bank account as a security for the contract, so it should have already been recorded as a separate journal entry with a credit to “Checking” and a debit to “Earnest Money.” For recording it here as part of the new purchase, you will utilize “Earnest Money” with a credit amount.

Line 4-7: Prorations and OpEx

Prorations of rent and/or operational expenses or CAM (Common Area Maintenance) are usually part of a commercial real estate transaction. These amounts are normally portions of rent that are “given” to you in the transaction. Typically, it reduces your liability against the asset. This can go into Accounts Receivable. This account requires a “Customer” to attach it to, so you will need to have the new tenants in QuickBooks already.

Line 8 and 9: Security Deposits

Leases often transfer with the property, so the transaction usually includes the security deposits. Separating each deposit by unit makes it easier to track and return to the correct tenant when needed.

Line 10: Closing Costs

As far as your title costs, bank fees, legal fees, etc., you can either break those out into separate accounts or lump them together in a “Closing Costs” account. You enter this as a debit, as it is part of the initial cost of the building, but is not part of the purchase price. For details on how to enter this as separate entries, refer to Hector Garcia’s video QuickBooks Online 2019 Tutorial: Recording a Rental Property Purchase, where he explains this in more detail.

NOTE: Please reach out to your tax accountant for further instruction on how to address the fees associated with the purchase of property.

Additional Tips for the Journal Entry

Recording the purchase of a fixed asset in QuickBooks is easy once you understand the steps outlined above. Then, read below for a couple of extra tips that will help you complete the process.

- Don’t forget to make a memo – just a small description with transaction information!

- Use the attachment function to upload the Settlement Statement to the Journal Entry. This will save you time at the end of the year or anytime you need to the uploaded records. You will not have to dig through your file cabinet, thumb drive, or online storage next time you need to see them.

Bookkeeping for Real Estate Investors: Best Practices

As far as how to enter an asset in QuickBooks goes, real estate investors must treat each piece of property as its own business. By breaking down every building, piece of land, or improvement into a separate category, it’s easy to determine which properties are doing the best and where costs are piling up.

Good bookkeeping isn’t just about data entry; it’s about insight. With fixed asset management software QuickBooks users can track loan payments, monitor depreciation, and keep records of upgrades or repairs with just a few clicks. If you’re using the online version, learning how to add an asset in QuickBooks Online ensures everything stays organized in real time, no matter where you’re working from.

The goal is to manage fixed assets in a way that keeps your books tidy, accurate, and in tax season or investor review readiness. Master this, and you’ll have fewer hours spent going back and correcting errors, and more time creating your real estate investment portfolio with confidence.

Interested in learning more about using QuickBooks for Commercial Real Estate? Check out our article and video on “Setting up a Chart of Accounts for a Commercial Real Estate Company.”