Accurately tracking prepaid expenses is one of the most crucial aspects of financial management for landlords or owners. Prepaid expense accounting ensures precise reporting and hassle-free reconciliation of Common Area Maintenance (CAM).

It’s a challenging task, though. Many landlords/owners find themselves entangled in the complexities of recording these expenses, leading to financial discrepancies and reconciliation headaches.

Mastering the art of categorizing and automating prepaid expenses takes time, but it can transform accounting from a time-consuming chore into a seamless process. With the right approach, landlords can sidestep costly discrepancies, maintain financial clarity, and keep their operations running smoothly.

Let’s explore the best practices for managing prepaid expenses in real estate, leveraging powerful tools like QuickBooks and automation solutions like STRATAFOLIO that bring efficiency and accuracy to the forefront.

What Are Prepaid Expenses in QuickBooks?

Prepaid expenses are charges made in advance for goods or services used over time. Typical examples in real estate include maintenance contracts, property taxes, insurance, and utility deposits.

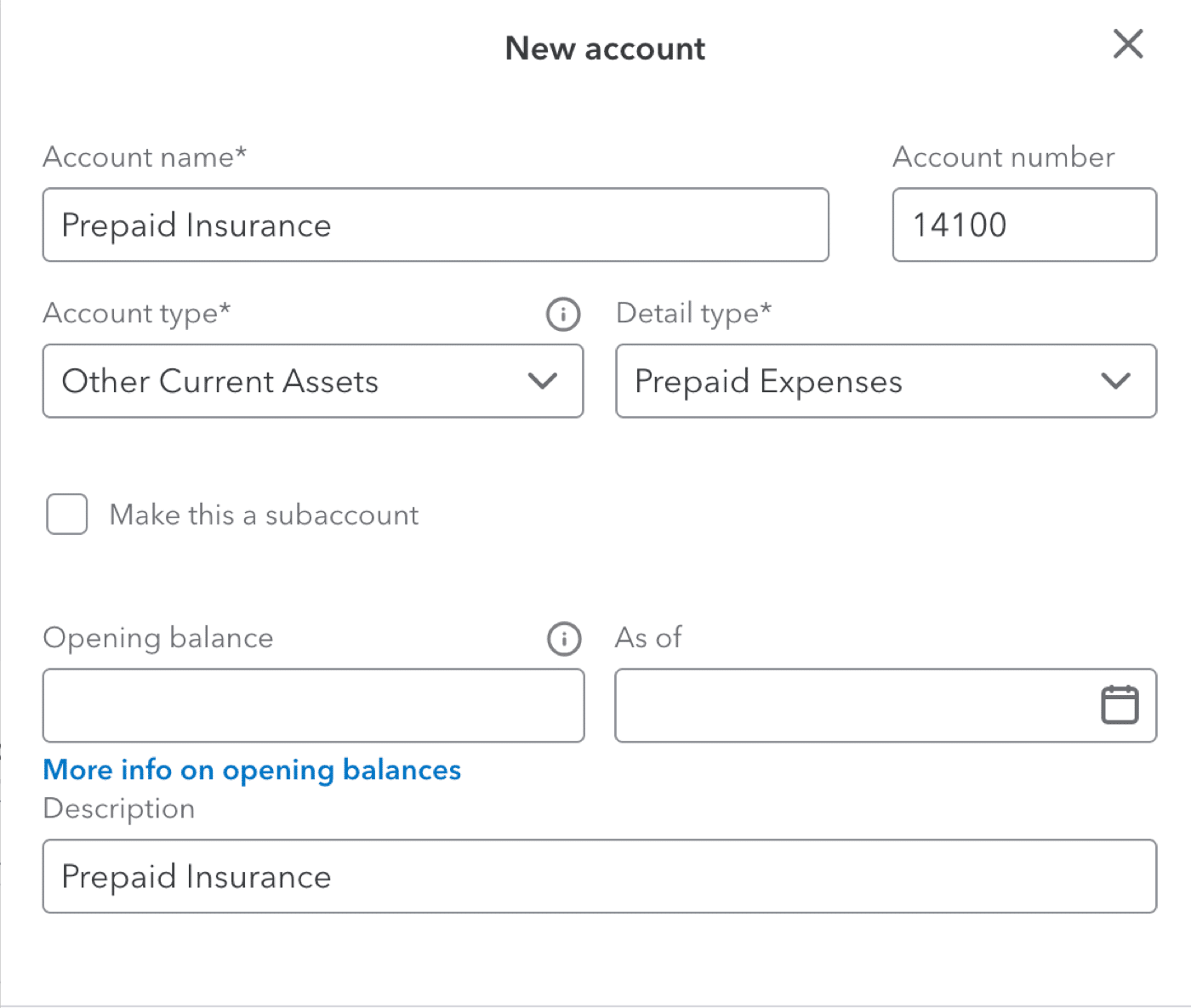

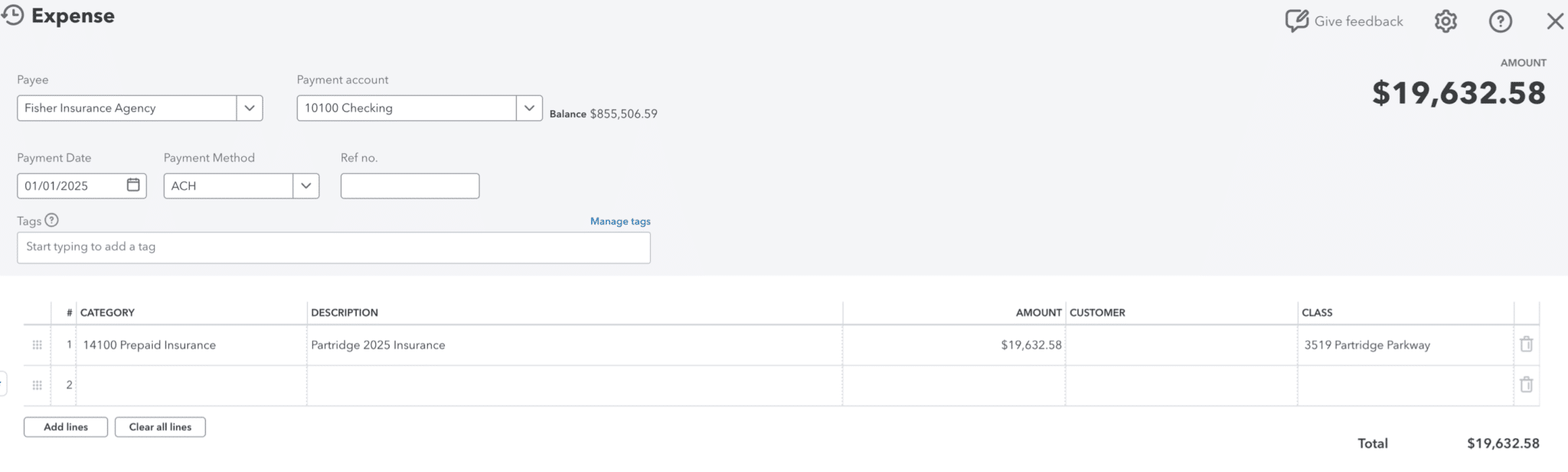

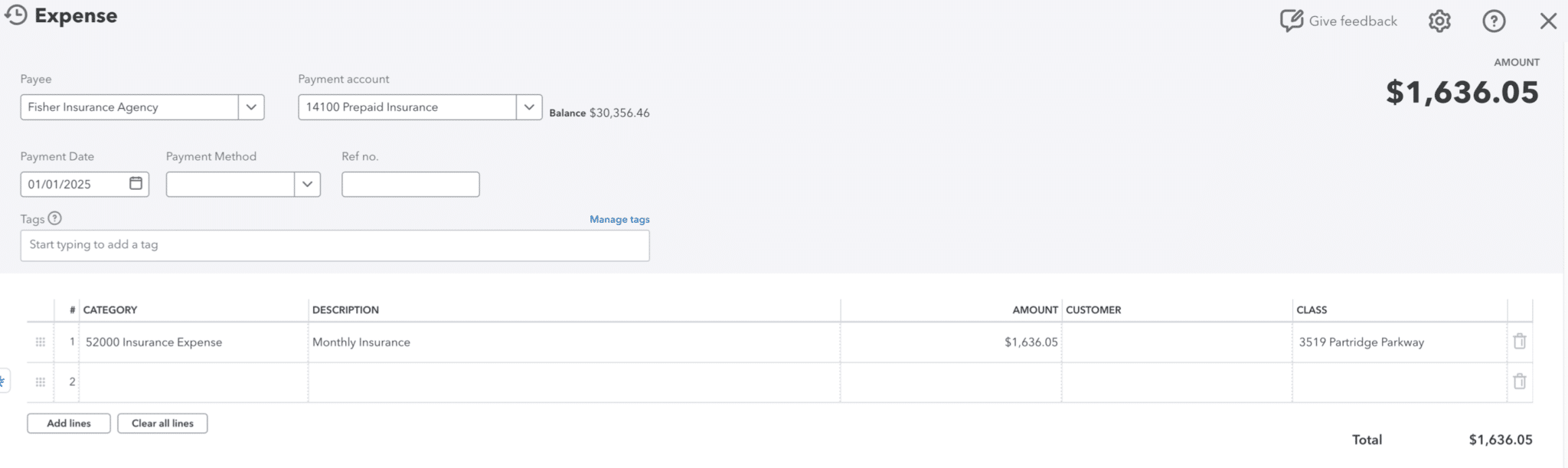

Prepaid expenses are initially recorded as assets on a landlord’s balance sheet and gradually become expenses as they’re utilized. In QuickBooks, these expenses should be recorded in a dedicated asset account to ensure accurate financial tracking.

For instance, if you pay for a year’s worth of property insurance upfront, you would record the full amount in the prepaid insurance account. Each month, a portion of this insurance cost is moved from the asset account to an expense account, reflecting the actual usage over time.

Tracking prepaid expenses correctly is critical. It assures a transparent view of your ongoing financial obligations and prevents distorting your Income Statements or Profit and Loss Statement (P&L) with lump-sum expenses. Plus, it will also help with mid-year CAM reconciliation, as we will discuss later.

Automate Prepaid Expenses Directly Inside QuickBooks Online

Automation significantly simplifies the process of tracking prepaid expenses. QuickBooks Online enables landlords to set up recurring journal entries that automatically allocate a portion of prepaid monthly expenses. This reduces manual data entry blunders and ensures financial reporting consistency.

By automating prepaid expense tracking, property owners can:

- Ensure accurate month-to-month financial reporting.

- Reduce the risk of missing or misallocating expenses.

- Save time by eliminating the need for manual journal entries.

Integrating a tool like STRATAFOLIO improves automation by providing advanced tracking features that align prepaid expenses with CAM reconciliation. Using this combination of software yields substantial benefits for commercial real estate owners.

For one thing, software significantly reduces human error. If you have 50 tenants, hand-calculating each pro-rata share and expense allocation invites mistakes, whereas software will do it consistently every time.

Automation also saves time. Tasks that used to take days to compile invoices and crunch numbers can be completed in minutes once the data is in the system. This frees up your team to focus on reviewing results and exceptions rather than doing math.

Another benefit is real-time insight. Many systems let you see throughout the year how actual expenses compare to the budget and even forecast whether tenants are overpaid or underpaid, so you’re not in the dark until year-end.

Remember when we mentioned the word CAM reconciliation? If you use pre-paid expenses correctly and your tenant leaves partway through the year, reconciling what is owed to or from the tenant will be much simpler. You will know what portion of the significant ticket expenses (taxes and insurance) the tenant should have paid, plus you will see the actuals for the other operating expenses for the portion of the year that has passed. STRATAFOLIO makes this particularly simple with our 1-click CAM reconciliation. But if you are manually calculating, the same mechanics apply.

What Type of Account is a Prepaid Expense?

Prepaid expenses appear under the asset section of the balance sheet rather than as an immediate expense on the P&L. These accounts show future monetary benefits that will be recognized over time.

Key prepaid expense accounts in real estate include:

- Prepaid Insurance: Covers property or liability insurance paid in advance.

- Prepaid Property Taxes: These are taxes paid before the due date but covering future periods.

- Prepaid Maintenance Contracts: Covers services like landscaping or security that are paid upfront.

Understanding where prepaid expenses fit in the financial statements ensures accurate bookkeeping and aids long-term financial planning.

Why Accrual Accounting Works for Prepaid Expenses

Landlords/owners can choose between cash-basis and accrual-basis accounting for financial records. The core difference lies in timing. Cash accounting recognizes income when cash is received and expenses when money is paid. In contrast, accrual accounting recognizes income when earned and expenses when incurred, regardless of actual cash movement.

Each method has implications for recording real estate transactions such as rent, property expenses, and prepaid charges.

Cash vs. Accrual

On a cash basis, the financials reflect actual cash flow. For example, if a tenant pays three months of rent late in one lump sum, cash accounting records all that rent revenue in the month it was received. Similarly, if you pay an annual insurance premium in January, the entire payment is recorded as an expense in January under cash accounting. This method is straightforward. Your books show money in and out as it happens.

Under an accrual basis, revenues and expenses are recorded in the period they happened in, not when money changes hands. Rent is recorded in the month it is earned even if the tenant hasn’t paid yet, creating an Accounts Receivable (A/R) until the cash comes.

Expenses are matched to the period of benefit. If you paid that annual insurance in January, under accrual, you would record one-twelfth of the expense for each month as the coverage is “used.”

At the time of payment, you’d increase a prepaid asset account rather than expensing it all. The result is that each month’s P&L statement reflects the insurance expense for just that month rather than a massive hit in January and nothing thereafter. Accrual thus normalizes expenses and revenues to the period they relate to, giving a more consistent view of financial performance.

The Advantages of Accrual

Most small landlords/owners often stick with using a cash basis, as it’s straightforward and meets their needs. Accrual accounting is generally the better choice for larger real estate businesses or any that require formal financial reporting because it provides a more accurate and meaningful view of financial performance.

QuickBooks provides the capability to easily switch between cash basis and accrual accounting, depending on your needs. Often, owners toggle between cash basis and accrual basis in order to evaluate different decisions.

Why are Prepaid Expenses Important in CAM Reconciliation?

Prepaid expenses play a crucial role in CAM reconciliation. Many real estate expenses, such as property taxes and insurance, are considered operating expenses landlords recover from tenants through CAM charges. If prepaid expenses aren’t tracked correctly, CAM reconciliation becomes inaccurate, leading to disputes or unexpected costs.

By setting up prepaid expenses properly, landlords can:

- Provide tenants with predictable “additional rent” charges each month.

- Ensure transparency in CAM reconciliation, reducing tenant disputes.

- Maintain accurate financial records, making audits and reporting more straightforward.

- Easily pull a report of the expenses (at any time) that should be allocated to a tenant.

The concept of prepayment is inherent to CAM reconciliation. Tenants prefer predictable monthly payments rather than unpredictable bills, and landlords use those payments to cover ongoing expenses.

At year-end, prepaid expense accounting and CAM reconciliation converge. A landlord’s books should accurately reflect all expenses (including allocated prepaid) for the year. Tenants should be charged exactly their share of those expenses, no more or less.

Sound prepaid expense management directly supports a smooth CAM calculation, ensuring the numbers used in reconciliation are correct and fair.

Record Your Prepaid Expense Using QuickBooks with STRATAFOLIO

STRATAFOLIO offers a seamless way to track prepaid expenses and integrate them with QuickBooks. By using STRATAFOLIO, property owners can:

- Automate the allocation of prepaid expenses through seamless syncing.

- Performa 1-click CAM reconciliation.

- Gain a more transparent financial overview through advanced reporting features.

Investing in capable commercial property management accounting software is a savvy decision for a real estate business that wants to improve its expense management. Features like automated CAM reconciliation, prepaid expense scheduling, and budgeting tools directly address owners’ most common financial management pain points.

Choosing a solution like STRATAFOLIO that fits your portfolio’s needs reduces the administrative burden of CAM reconciliations and prepaid tracking. This yields more reliable financial reporting and smoother audits, contributing to better tenant relations as charges become timely and accurate. This ultimately supports the economic health and professionalism of your real estate business.