Have you taken out a mortgage recently and established an escrow account? Our blog reviews what an escrow account is and how you should set it up properly in QuickBooks. Read on for the details!

What is An Escrow Account?

When you borrow from a lender, lenders often offer to create an escrow account for you. The escrow account is established to cover costs associated with taxes and insurance. The lender manages this account for you and sends periodic statements of the activity.

Lenders like escrow accounts because it gives them peace of mind that your taxes and insurance will remain current.

Simply put, an escrow account is a way for you to put a little money aside each month to cover taxes and or insurance for when they are due. When you make your monthly mortgage payment, a portion of it will go to your principal and interest, and another piece will go towards your escrow account.

Your lender estimates your taxes and insurance costs for the full year and splits it evenly across the 12 months. Periodically, adjustments will be made to your escrow account to cover increases or decreases in insurance or taxes.

When the insurance and tax payments are due, your lender will make the payments. Then, reduce your escrow account by the amount paid to the tax assessor and insurance company.

How Should I Set up the Escrow Account?

There are two primary ways people set up their Escrow Account in QuickBooks – as a Bank Account or as an Other Current Asset. Either way is acceptable. Both have the same effect on your Balance Sheet and Profit & Loss Statement. It comes down to personal preference.

Our preference is to set this up as a Bank Account as seen in our recent blog, How to Set Up a Chart of Accounts for a Real Estate Company. We prefer the use of bank account because it is money we have set aside in a checking-like account, to cover expenses. And, as we pay the insurance and taxes expenses, our balance goes down. As we make deposits, our balance increases. It is important to note, whether you use the Bank Account or Other Current Asset to record escrow, the transaction is happening with your lender. The escrow account you set up is to mimic the transactions with your lender.

Setting Up Escrow As a Bank Account

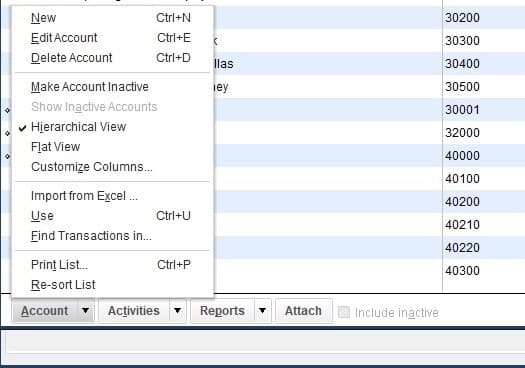

Here are the steps to set the escrow account as a Bank Account in the desktop version of QuickBooks:

- Go into your Chart of Accounts.

- Select Account on the bottom left-hand side of QuickBooks and select New.

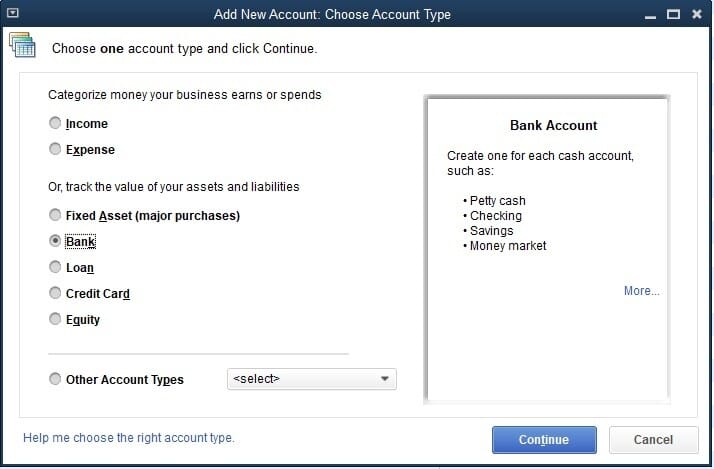

3. Select Bank, then Continue.

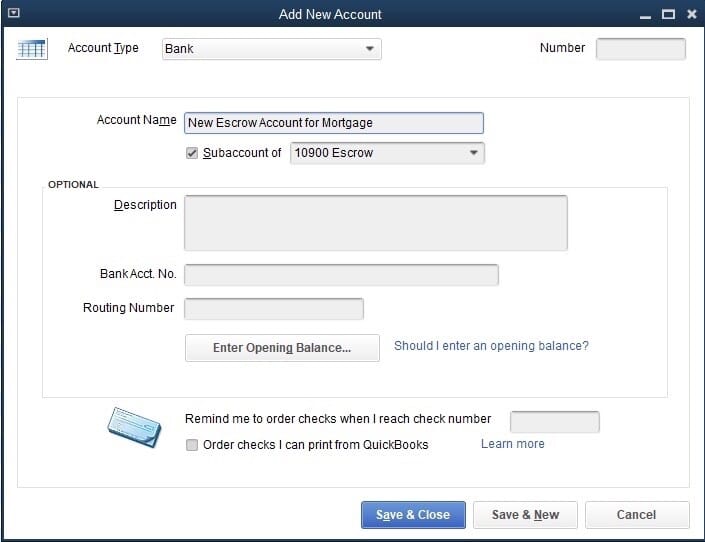

4. Create a new account under the subaccount escrow for your new mortgage. Likely you will want to associate with the property you purchased.

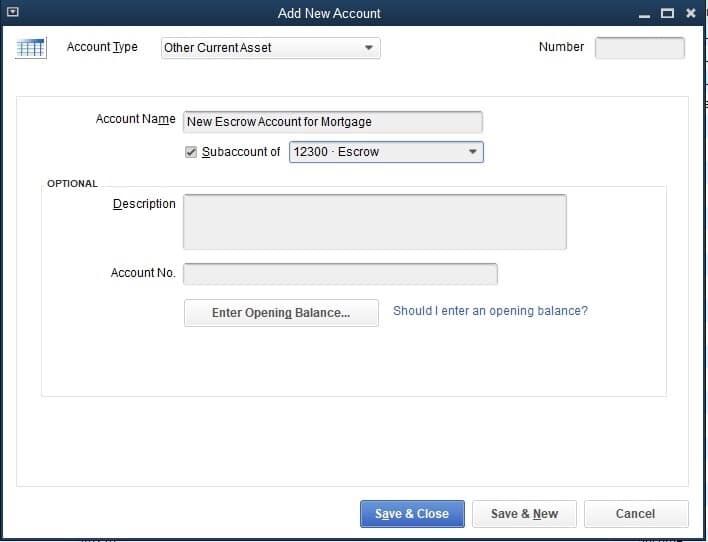

Setting Up Escrow As Other Current Asset

Setting up the Escrow as an Other Current Asset is a very similar process. Steps 1 and 2 will be the same.

- Same as step 1 above. Go into your Chart of Accounts.

- Same as step 2 above. Create a new account.

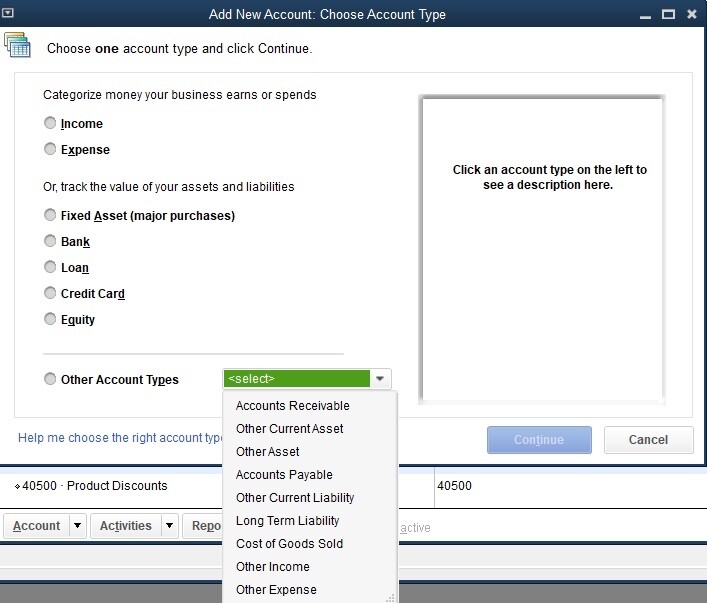

- Select Account Type Other Current Asset from the drop-down menu.

- Finally, create a new account under the subaccount escrow for your new mortgage. Likely you will want to associate with the property you purchased.

Conclusion

Setting up the escrow account is fairly straight-forward once you know the basics. And, there are many ways to accomplish the same thing. The key is consistency. For more information on setting up your recording your mortgages correctly, check out this video and blog.

And, if you are new to QuickBooks or want some other suggestions on how to set up your QuickBooks correctly from the beginning, schedule a demo to get you started!